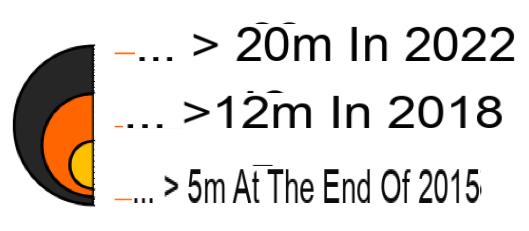

The latest telecommunications observatories show a certain enthusiasm for fiber optic offers. Promising much higher speeds, very low latency, and unparalleled stability, fiber is a promise everyone expects, but few have yet achieved. True fiber or false fiber, we mean everything and its opposite. And a few months ago, Orange announced an increase in its investments in order to cover 20 million households by 2022. A very ambitious objective which prompts us to revisit this technology which should soon entirely replace this old pair of copper used by ADSL and cable.

In recent months, we have talked a lot about the arrival of 4G in our territory. Supposed to accompany the explosion of Internet uses, the principle of this technology is to increase the capacities of relay antennas in order to provide higher speeds to users. However, it alone does not cover all current and future fixed uses: downloads of large files (games, OS updates, etc.), 3D and / or 4K television, cloud. If 4G provides the expected comfort for mobile navigation, fiber will be its equivalent at home to provide the necessary speeds in the future.

Our goal here: to start from scratch. There are many questions and their answers are often vague. If fiber is becoming so obvious - even though DSL connections still satisfy many customers - it is mainly because Internet uses are exploding and the copper pair is reaching its technical limits. It is also necessary to understand how the deployment of this fiber which interests so much takes place. Between a complex term and obscure cover cards, eligibility does not seem so easy to decipher. This report will therefore come back to the terms used and the deployment objectives set by Orange (the leader in deployment in Spain), but also on point-to-point (P2P) and point-to-multipoint (PON) architectures. , in order to better understand the construction of the local loop, that is to say the final part of the network which connects users to the operator's connection node.

The best Internet Boxes

Fiber, RED box Fiber Cable

Fiber, RED box Fiber Cable 5 days

Speed up to 1 Gb / s

35 TV channels included

Telephony to 100 destinations

€22€35

Discover

Fiber Bbox must Fiber

Fiber Bbox must Fiber 2 weeks

Speed up to 1 Gb / s

180 TV channels included

Telephony to 110 destinations

For 12 months € 15,99€39,99

Discover Fiber, SFR Fiber Limited Series Cable

Fiber, SFR Fiber Limited Series Cable

Speed up to 500 Mb / s

160 TV channels included

Telephony to 100 destinations

For 12 months € 10€38

Discover All internet boxesAs you will have understood, the subject is particularly vast. Make yourself comfortable, let's go for a complete overview of this fiber that fascinates Internet users of all stripes.

The explosion of traffic and usesFiber is quite simply a necessity today. It is not just a simple evolution, a marketing creation or a geek product. Faced with an aging copper pair which was not initially intended to cover as many uses as is currently required (video streaming, downloads, online games, etc.), fiber is emerging as the revolution for the next few years. Internet needs are increasing and demand is growing: fiber is presented as the only solution to support the rise in uses, which are more numerous and more demanding, and which are emerging day by day.

Because yes, it's a fact: content is becoming more and more greedy. Whether it's downloading multi-GB updates, demanding games or HD / 4K videos, the bandwidth of DSL connections is becoming more and more limiting. It ends up recalling the experience of the 56K of yesteryear, where it was necessary to launch downloads for whole nights! However, not all users have such intensive use. But, when each household has an increasing number of connected devices, then the use of the bandwidth becomes more and more regular, even if each device does not make a very massive use of it.

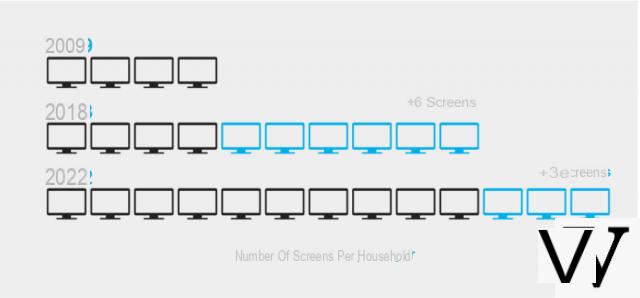

While there were on average four screens per household in 2009 (TV, smartphone, computer or tablet), there will be 10 in 2018 and 13 in 2022. Add to this the countless connected objects that appear on the market and which will multiply in homes over the next few years (surveillance camera, connected TV, connected scale, connected refrigerators, etc.). In the end, the downloads are more and more heavy and more and more numerous thanks to the multiplication of the devices which surround us. Average consumption increases over time: we are talking about an increase of 50% per year.

Number of screens per household

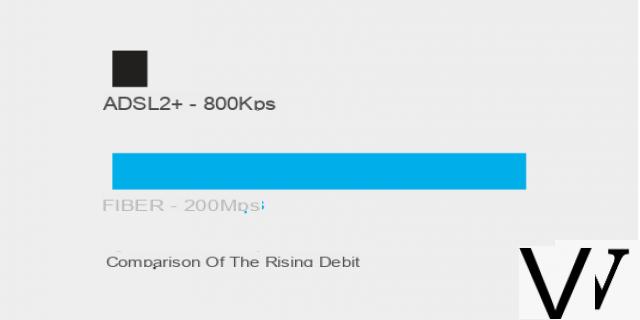

New uses are also emerging and require more and more bandwidth in the opposite direction (it is then a question of sending data from the device to the servers): teleworking, content sharing via social networks or using the cloud for gaming or file storage. These uses are becoming more and more unavoidable and suffer from bandwidth limits in this upward direction (or upload) imposed by the asymmetric technology of ADSL2 +, whose upstream speeds are much lower than downstream speeds (800Kbps vs 20Mbps). This attraction for these new uses (amounts) can also be observed in certain countries where the fiber is more developed (such as Japan) where we can observe an explosion of upward flows, which have become more important than downward flows (the downloads). It's a real change in behavior.

Copper limits have already been reached

The copper pair that allows us to connect to the Internet today is reaching its technical limits (in terms of speeds) and its reliability is becoming more and more a problem for many customers. It should be remembered that at the start, the copper pair was intended above all for telephoning. At that time, copper was a good enough alternative to replace string and cups. Except that today, the signal traveling in these cables contains much more information than initially, the signal therefore emerges much more sensitive to imperfections in the installation.

Every electromagnetic disturbance along the line becomes a real problem; the circulating electrical signal is very sensitive to the vagaries of the environment, it recovers all the surrounding imperfections (a defective power strip, for example) and desynchronizations (losses of the Internet connection) can then occur in an untimely manner. This becomes particularly troublesome on installations which are also aging. For the manager of this historic network (Orange), the annual cost for the maintenance of the network alone is estimated between 150 and 200 million euros.

Thousands of pairs of copper that are becoming more and more difficult to maintain

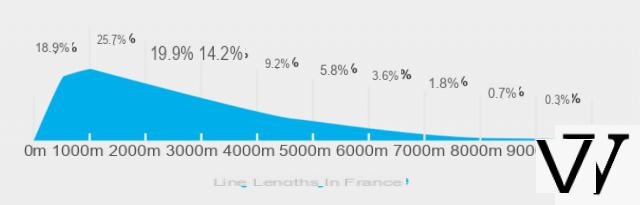

The various disturbances are unfortunately not the only constraints. The distance of the lines is another, and of size. The electrical signal which circulates along the lines is attenuated because of the resistance, a law of ohm far from being negligible since the signal becomes unusable after 6 or 7 km. Mitigation is the biggest problem in deploying the Internet for all. This weakening of the signal is observed in particular via the significant loss of bandwidth observed from the first kilometer: as a result, a large part of the subscribers cannot reach the theoretical speeds promised by ADSL (2+) technology.

For the example of Paris (the most dense area with 36 nodes of subscriber connections - the telephone exchanges where the subscribed lines meet), a third of the subscribers do not have access to High Definition TV by ADSL. Nationally, this weakening over the miles makes many households ineligible and limits the access of thousands of others to connections not exceeding one Mbps.

In the end, the average flow rates for all households (the closest as well as the furthest from the connection node) will be the main limit for copper in the coming years. The downlink speeds (downloads) have reached their theoretical limit since the only future advances (G.FAST in particular) will only concern the first meters after the node of subscriber connections (nevertheless useful for an increase in intermediate speed). As for the uplinks (sending data), they are very limited (0,720Mbps) for ADSL2 + and prevent the development of many uses.

Copper is dead, long live the fiber

Faced with all these drawbacks, fiber seems ideal to cover our future needs. Unlike the copper pair which circulates an electrical signal sensitive to electromagnetic disturbances, the fiber transmits light. The advantages are multiple: very low latency, high data rates, insensitivity to environmental disturbances and extremely low attenuation.

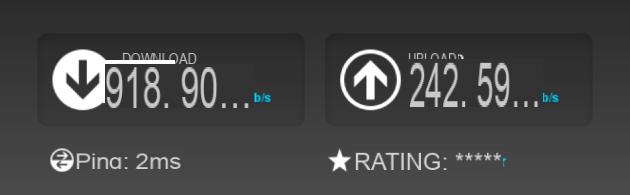

Throughput and latency are undoubtedly the most important elements for the years to come. The latency - a factor which influences in particular the comfort of navigation - is much lower than that of copper, in particular because the signal propagates at approximately 60% of the speed of light in a vacuum, that is to say 200 000 km / s for current fiber, consistently over very long distances (error correcting codes and buffers needed for copper are expensive in latency). Thus, the observed Ping value is generally 1 to 2 ms.

Speed test carried out with an Orange Fiber JET offer

Regarding flow rates, they are out of step with those of copper technologies. Current commercial offers offer downlink speeds of the order of 1 Gbps, i.e. 50 times more than an ADSL2 + connection and 10 to 20 times more than a VDSL connection, regardless of the distance from the subscriber to the connection nodes, since the loss per kilometer is negligible unlike DSL technologies (although other factors, couplers among others, can nevertheless have an impact on the loss, we will see later). In the upstream direction, the speeds are even more impressive since they are up to 300 times higher (200Mbps) than the speeds of a good ADSL2 + connection, and this, always regardless of the distance to the connection node.

Flow comparisons

The speeds are thus much higher than the best speeds of current DSL technologies, even though the latter will only be obtained for only 10% of the subscribers closest to the connection node. To compare, it is therefore also necessary to take into account the average distance of the DSL lines because, in fact, the average DSL speeds observed are far from being at the level of the announced speeds: they are rather of the order of 8-10 Mbps in average over the whole of Spain, a point which contrasts with the minimum 100Mbps offered to any fiber customer (FTTH - Fiber To The Home).

Distribution of copper lines in Spain (source DegroupNews)

In addition, the theoretical limits of fiber are far from being reached since tests at Orange have already made it possible to pass several Tbps in a fiber over several hundred kilometers. Thus, the use of fiber seems sustainable.

New world record for optical transmission for the @orange 38,4 Tbp / s network on 32 channels transported over 762 km @mno_jl #fibre #saser

- Jean-Luc Vuillemin (@jlvuillemin) June 23, 2015

In addition, the capacities of the fiber allow a significant gain in space, firstly because it is much thinner (the size of a hair) than the copper pair, but also because the flow rates that it allows. make it possible to supply 64 customers with the same fiber on the local loop, that is to say the network between the customer and the operator's central office.

A copper cable of 900 customers is equivalent to 15 fibers the size of a hair!

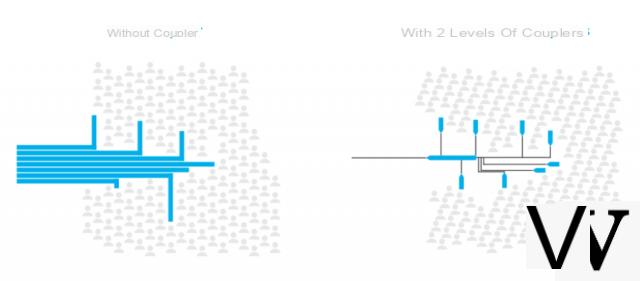

From the point of view of civil engineering, this saves space and saves time since it is not mandatory to pull a large number of fibers for the deployment of a given area - we will come back to this later. Concretely, in the city of Paris, the number of connection nodes will drop from 36 for copper to 6 for optical fiber. That's a lot of square meters freed up, which ultimately has an impact on costs. The following illustration allows us to understand the advantage of not deploying one fiber per customer (via the use of couplers which split a fiber into several fibers).

Use of couplers for fiber deployment

Getting rid of copper will also be an excellent source of savings - 150 and 200 million euros per year for maintenance alone, already - and its resale will also bring in a lot. A study of the sidewalks in Hauts-de-Seine (92), for example, estimated the weight of copper in the local loop at 50 million euros. However, this divestment from copper will not take place for 5 to 10 years after the deployment of fiber. Many conventional lines for telephones, alarms or elevators will need to be replaced first.

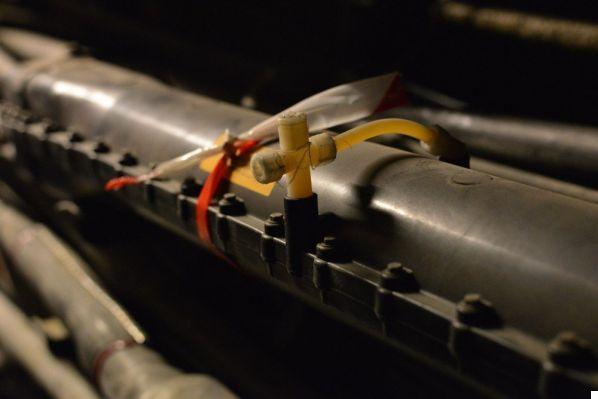

In addition, the use of light makes it possible to use reflectometry techniques to identify the location of problems on the network, which is much more precise than the air injection-based techniques used until then for the copper.

Module with which air is injected to locate a problem on the copper network

In the end, fiber brings enormous benefits for the customer, who benefits from much higher speeds and a much more stable connection (apart from shoveling on the roads, etc.). This can also be seen through the consumption of subscribers which jumps when switching to fiber: their consumption is generally doubled.

Deployment objectiveIn Spain, we have been talking about the deployment of fiber for years, but with the months lost to set the rules for engineering and pooling, investment has only recently accelerated. Before going into the details of the numbers, it is important to clarify some vocabulary elements.

Understand the deployment in a few terms

Deployment maps are often misleading: they show us extremely wide areas of coverage, but not quite what we expect. The areas covered are those where the fiber is deployed in the streets or in the neighborhood (the local loop): housing on the street is then said to be addressable. Unfortunately, and this happens in many cases, a neighborhood covered by fiber does not mean that all residents can subscribe to a fiber offer.

In fact, to take advantage of the fiber, the accommodation (or the pavilion) must be connectable, that is to say that the fiber is deployed in the building (with connection points on each floor) or that the suburban streets have connection points. In this case, there is a pooling point upstream (at the bottom of the building or in a street cabinet) to which the commercial operators who cover the area will connect. We will come back to this in more detail later.

If a home is connectable and an operator covers the area (and has connected its local loop to the building's pooling point), then the customer is said to be eligible to the fiber offer of this operator. When the customer wishes to subscribe, the fiber is then drawn from the connection point (on the landing of the building or in the street for the pavilions) to the interior of the accommodation; the accommodation is then connected. We note that this final connection takes place only when the owner or tenant signs a first fiber contract.

Issy-Les-Moulineaux, soon the second city to be fully fiberized

State of deployment in Spain

Today, fiber is still in its infancy (in Spain): on June 30, 2015, there were approximately 4,7 million homes eligible for FTTH (Fiber to the Home) on more than 30 million copper lines: the effort to be made is therefore still significant. The Very High Speed Plan plans to cover 80% of households with FTTH by 2022, and the remaining 20% via speed increase techniques (speeds above 30Mbps).

FTTH = Fiber to the Home, or fiber to the home

When in 1975, the telephone catch-up plan was adopted, the objective was to deploy 14 million new telephone lines in 7 years. The objective set for fiber is therefore significantly more important, even though a major element complicates the task: competition. At the time of the monopoly, equalization was much easier via the increase in the price of subscriptions (as well as the State's investment).

Today, the investment is made with the money of the banks. It is now much more complicated, moreover, to undertake the necessary steps and negotiations with the communities and territories (at the time, the will of the State "was sufficient"). In the end, the cost of the investment to deploy fiber in all homes is estimated between 35 and 40 billion euros; the state wants to put between 4 and 5 billion euros for less dense areas, the rest will be mainly the responsibility of the private sector (and communities).

Orange, which is positioning itself as a leader in deployment

In this deployment of fiber, Orange is a driving force, as it aims to reach 12 million connectable households by 2018 and 20 million by 2022. This is a very ambitious objective that will be achieved in tripling its investments, which puts it in the first place of private investors with 3 billion euros planned for the period 2015 and 2018 (for Spain).

Orange's objectives in terms of the number of connectable homes (Orange illustration)

Orange is also positioning itself as the first operator to set itself the goal of making 100% of households in 9 Spanish cities, including Paris, Lyon and Lille, connectable. He carried out a first experiment in the town of Palaiseau where 100% of the housing units are now connectable. This experiment is a real success since the inhabitants show a real interest in the new uses and the new services that this allows.

Map of Orange's coverage targets by 2018

Making 100% of homes in a coverage area connectable is an excellent way to speed up the migration of customers from a given area (in Paris, for example, 35% of homes remain non-connectable even though fiber has been present there for several years. ). In fact, fiber is proving to be a powerful driving force in winning back new customers, which becomes an important objective for Orange when it is no longer the leader in fixed Internet in these very competitive areas (it does not have " that »30 to 35% of the market). Currently in terms of recruitment, 90% of new Orange customers are fiber customers: a fairly eloquent figure.

Moreover, while it now has a monopoly on copper, the construction of the fiber optic network concerns all private operators as well as communities. Orange will therefore not be able to control 100% of the fiber lines, as is the case today with copper. By investing in a massive way, it can nevertheless hope to take a big share of the pie (an objective of 80%) in order to keep its leading position with the general public.

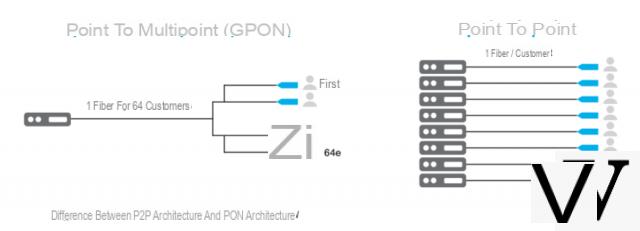

The PON architecture, a genius advantage

THEarchitecture P2P (point to point, that is to say an end-to-end fiber per subscriber) is already known to all since it is the technique used for the deployment of the telephone via the copper pair. There is a copper pair from each housing to the connection node, and therefore a substantial infrastructure to deploy. Its drawbacks are therefore quite observable through the current copper local loop: the connection nodes where the customer lines meet are quite numerous (there are 13000 of them in Spain) and are generally of large size since the copper cables are very bulky. (see photo below) and the different equipment is to be multiplied by the number of customers. This P2P architecture, although natural for users who expect to have a dedicated connection, is not the most optimal.

In the basements of the connecting nodes, hundreds of cables the size of an arm ...

Today, the capacities of fiber make it possible to consider other much more practical and economical methods where the same fiber can be shared by several users: this is the point-to-multipoint PON (Passive Optical Network) architecture. The final connection is identical: each household has its own fiber. On the other hand, between the home and the connection node, the use of couplers in the network makes it possible to share the information passing through a fiber between 64 clients, as we mentioned above. In the end, 64 customers receive the same light signal. The data is therefore encrypted upstream and then “separated” by the customer's final equipment (by the ONT).

Already existing bottlenecks

Even if this approach consisting in sharing the same link may surprise more than one, it is a technique nevertheless common in collection networks. For example, the interconnections between the operators and the servers of the online platforms (Facebook, Google or even Netflix) are already shared between the users (no dedicated fiber for each user or subscriber to the service). Thus, even if we do have a dedicated copper pair from the home to the connection node, this is no longer the case on the upper part of the network where the links are shared. If the interconnection is well dimensioned, then the user does not perceive any slowing down or saturation phenomenon; conversely, undersizing can cause slowdowns even for customers with a high performance dedicated connection.

In concrete terms, the risk of saturation for the PON architecture is, statistically, almost zero since the GPON currently used allows speeds of 2,5 Gbps in the downstream direction and 1,25 Gbps in the upstream direction (shared by the 64 clients) . These figures may seem low, but we must not forget that greedy uses do not occur at the same times and are relatively rare (few greedy customers in the end). They are also limited in bandwidth, leaving enough space for all users. In addition, in the event of proven saturation of a fiber, the operator can very easily double the bandwidth (by switching half of the subscribers to a new card at the optical connection node).

In practice, current speeds are largely sufficient since Orange is able to guarantee fairly high minimum speeds for its offers: 500 Mbps for its premium offer. It then effectively offers speeds greater than those it promises: 1 Gbps instead of 500 Mbps. In practice, the P2P architecture therefore does not provide more in terms of speeds. It should also be noted that the speeds shared between the 64 customers will soon be able to be multiplied by 4 thanks to 10GPON and that other technologies to come will allow even more dazzling increases in speed.

Difference between P2P architecture and PON architecture

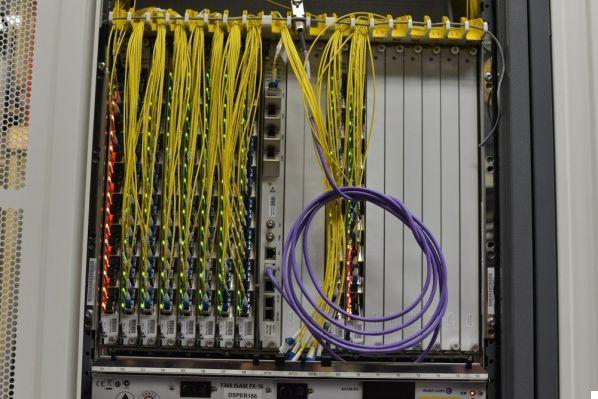

The advantages for the optical connection node

From an infrastructure perspective, the advantages of PON are manifold. On the one hand, the use of couplers makes it possible to optimize the civil engineering since a very limited number of fibers leave the connection node. On the other hand, the devices of the connection node take up much less space since the clients are grouped by 64 as can be seen in the illustration above (roughly, we could say that the number of devices required is 64 times less important). Thanks to the following two photos, we can distinguish the difference in space used between the current copper subscriber connection node (in P2P) and the PON fiber equipment.

The copper connection node for the 67000 housing units in Levallois

And its fiber equivalent ...

The equipment at the Optical Connection Node (NRO) is called the Optical Line Termination (OLT) and is the interface between the collection network (the top of the network) and the optical network to the customer (the loop local). The vertical modules (see photo) are the PON cards where each port manages 64 clients. The best OLTs can manage 8 ports per card, or 512 clients. PON equipment is more expensive than P2P equipment, but space and civil engineering savings remain in favor of PON since P2P is at least 30% more expensive. Apart from this equipment, the rest of the network up to the subscriber is passive. In the event of an increase in flow, it is therefore sufficient to intervene on these OLTs.

Optical Line Termination (OLT), the DSLAM equivalent of ADSL

The PON architecture also makes it possible to limit the number of NROs for the same town since the equipment is less bulky and the distance between the customer and this node is no longer as important. The signal attenuation per kilometer is negligible (especially compared to copper), and only the couplers have an impact on this attenuation. Thus, 6 optical connection nodes are sufficient for the city of Paris, instead of 36 NRA for copper: a huge gain in space! For Free, which has chosen P2P (the only one), the number of NROs should therefore be much greater (probably 70).

The use of couplers

The use of couplers makes it possible to split a fiber into several fibers. The idea of PON is to start from one fiber and get 64 in the end. To optimize the deployment of the local loop, a first level of coupler is positioned from the NRO (1 to 2 fibers).

The advantages are multiple: a thinner tree structure (branches of the tree with 32 clients instead of 64), fewer couplers in the local loop, which facilitates deployment while reducing costs and allows the addition of a second OLT on the shaft (allowing two technologies to be combined on the same fiber). In this situation, the range with all the couplers is only 10,5 km since each coupler causes attenuation. For more distant buildings, this first level of coupler is removed (32 customers per fiber in this case) and the range is 18,5 km.

Splice cassette where the couplers are located

Finally, the PON architecture has been favored by many operators in the world and in Spain for the speed of deployment and the lower cost of zone coverage, even if maintenance can prove to be more expensive and problematic (a problem on one fiber can affect several customers). The speeds theoretically offered by P2P are not in reality an advantage since the collection network is then often the limiting factor. In practice, Free does not offer higher speeds than those of Orange.

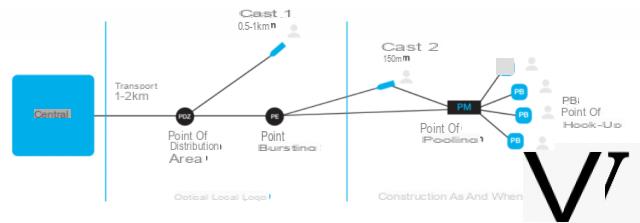

Stages of deploymentOptical local loop: plate construction

The optical network is built in plates, that is to say in zones of influence grouping for example the connectable dwellings of the same district. Each plate has a Zone Burst Point (or PEZ), the seat of the second level of coupling (the first being that of the NRO) where each fiber is exploded towards 8 fibers which are then distributed among the various important pockets of the plate. (streets, buildings, etc.). The bypass and coupling is done via a Splice Protection Box (or BPE, see photo). The PEZ is connected to the NRO by a (and only one) transport cable which can contain several tens of fibers. It is connected either directly or indirectly when the cable passes through a Splicing and Tapping Point (PEP) used to separate part of the fibers of the transport cable towards several plates.

Splice protection box

Between the PEZ and the housing, we can then find two points of convergence: the bursting points and the mutualisation points. The bursting or connection points (which correspond to a pocket of the plate) have no coupling function and only branch off part of the fibers to several sectors of the pocket. The last level of coupling takes place in the pooling points where all the housing units are directly connected (therefore with a dedicated link per housing unit).

Diagram of the local loop: a construction by plates

Points of mutualization

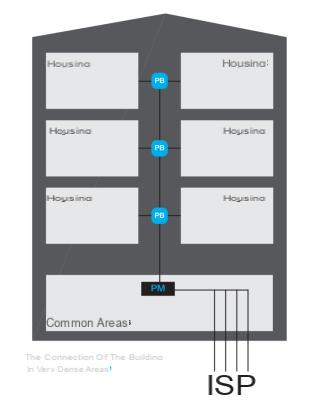

The point of mutualization (PM) is a key element since it is the interface between the local FTTH loops of the different operators and the mutualized fibers serving all the dwellings or pavilions. It is therefore on this point of mutualization that all operators connect. In each pooling point, the operators install their module which is then connected to their local loop. Then, each time you sign a contract or change operator, you just need to change the connectors.

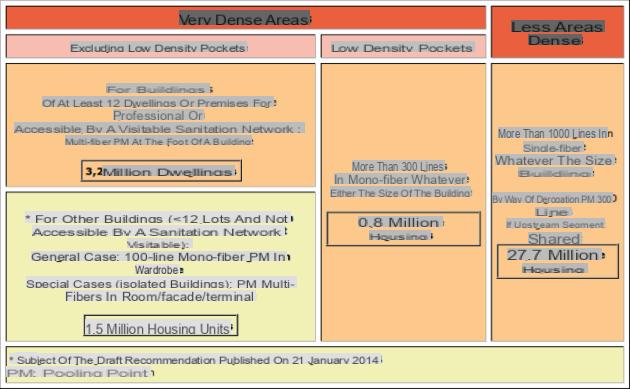

There are three types of PM depending on the density of the area: building pooling points (> 12 homes), street pooling points (for buildings with less than 12 homes) or area pooling points ( mainly serving pavilions).

ARCEP (the telecoms policeman) defines the use cases for each type of pooling point:

The different deployment zones defined by ARCEP

In sparsely populated areas or pockets of low density, the pooling points are located in the public domain and group together from 300 to more than 1000 lines. Downstream of the PM, a fiber is drawn for each dwelling and up to the connection point (PB) generally on the road. This connection point is precisely the point that differentiates connectable dwellings from connected dwellings: each customer who signs a first contract is connected to the PB via one (and only one) fiber. Here is an example of a zone pooling point (360 homes) deployed by Orange:

Zone pooling point (PMZ) to which between 300 and 1000 housing units is connected

In dense areas, there are street pooling points (PMR), for buildings with less than 12 housing units, for example (and not accessible by a visitable sanitation network). These are street cabinets on the public domain. Either these cabinets are connected to different buildings with less than 12 dwellings (up to 100 lines per PMR), and it is then monofiber, or the cabinet is installed for a particular building and it is then multi-fibers (four fibers per housing). The connection points are located on each floor of the buildings.

Street pooling point covering buildings with less than 12 housing units

Finally, the building pooling points are located inside buildings with more than 12 housing units. There is a branch point at each floor and the subscribers are then connected via four fibers.

Deployment of the riser in a building in a dense area.

In practice, the deployment of the pooling point and the entire downstream part is done by a single operator. In buildings, the choice of this operator is made by the trustees, when in sparsely populated areas, town halls or communities, for example, are responsible for it. Then, all operators can install their equipment there if they wish and if the area is covered by their local loop. In all cases, marketing is not possible within three months of the work so that the operator who deployed this shared part does not have an advantage. In fact, it is Orange which mainly deploys these common parts and 9 times out of 10, it remains the only operator after the three-month waiting period.

70% of homes that can be connected to fiber in Spain have been thanks to Orange

The operator responsible for deploying this shared part remains manager for a renewable period of 25 years. When a customer signs a subscription with a commercial operator connected to the PM, the latter can himself make the final connection to the customer's home (between the connection point and the home), but always under the responsibility of the managing operator. . The use of this network then gives rise to the payment of rent. It can therefore be an annuity for an operator who deploys the buildings on a massive scale.

The technology of the superlativeThe promises of fiber are quite numerous: better speeds, better latency, better stability. Many superlatives for this technology which should entirely replace the copper pair which currently connects us to the Internet. But deployment takes time, is very expensive and many are wondering about the arrival of this technology in their homes.

Today, Orange is positioning itself as a leader in the deployment of this fiber by setting the objective of making 20 million households eligible by 2022, far ahead of its competitors. Even more strongly, it will make 100% of the homes in 9 major Spanish cities connectable by the end of 2016. This will be done thanks to an increase in its investments and to the PON architecture, which makes it possible to deploy much more quickly. and economical than the P2P architecture previously used for copper.

This PON architecture surprises more than one since 64 customers share the same fiber, dividing by 64 the theoretical speeds of a fiber. However, the network is built in such a way that the speeds offered in PON at Orange are equivalent to those offered by Free in P2P. The architecture is therefore not the only element to be taken into account since the sizing of the collection network is an essential point (some Free customers report saturation on certain services, even though their dedicated connection is excellent). In the future, the bitrates are expected to increase again and again. Orange is currently testing 10GPON, multiplying the capacities of each fiber by 4. Other techniques are already under study and make it possible to envisage even more dazzling increases in speed, such as the use of wavelength division multiplexing (WDM-PON) allowing to have a dedicated wavelength for 1 or 2 clients. The best of both worlds between P2P and PON, in short.

Today, fiber offers are a success from a commercial point of view: the customer consumes more services with high added value (3D / 4K VOD or online storage for example) while accepting a move upmarket and increase in the price of the package (5 to 10 euros). But in this area, operators are not fighting with the same weapons: SFR offers fiber offers that are not really. The FTTLA offers (a local fiber loop but a coaxial termination) offer much better speeds than ADSL, but behind in relation to "real" fiber (especially on much lower uplink speeds) and in a heterogeneous way because all the zones do not offer the same speeds, unlike the majority of fiber offers. In addition, the advantages in terms of stability are then completely called into question for this technology since the copper terminal part (at the customer's site) remains sensitive to environmental disturbances. Will the customer be able to perceive this difference between FTTLA and FTTH? In reality, nothing is less certain.

Find more information on the deployment of each operator and the offers of each by following these links:

- Orange

- SFR

- Bouygues Telecom

- Free

This article was made possible thanks to Orange which opened its doors to us. If other operators want to tell us more about the technologies they use and their deployment, they can contact us using the form provided for this purpose.